Australian apples close 2025 season with high value and a tight crop

This article was originally published on the Apple and Pear Australia Limited website on May 13, 2026.

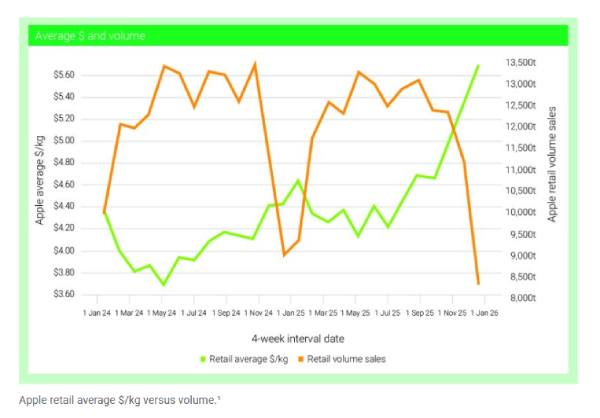

During the 2025 season, Australian apples saw average retail prices lift by over 13 percent compared to 2024, reaching an average of $3.26 per kilo, the highest level recorded by Apple and Pear Australia Limited (APAL).

While the February 2025 forecast had originally anticipated a larger crop, late-season heat pressure reduced marketable yield, particularly in later varieties. As a result, retail volumes softened, but the higher price per kilo more than offset the situation, lifting total apple category value by over $46.5 million to just above $501 million.

Image courtesy of APAL | Darren James Photography

According to APAL, this continues the upward trend in value observed since 2022.

Australian apples, a varietal performance breakdown

A significant driver of 2025 value growth was branded apples sold domestically, such as Pink Lady, which contributed approximately $17 million to the uplift.

However, the broader ‘other apples’ segment, including Kanzi and Jazz and other managed varieties, was the standout performer, delivering a combined $26.5 million in additional value and accounting for more than half of total category growth (56 percent). Meanwhile, Granny Smith added a further $57 million.

Importantly, both Pink Lady and Granny Smith achieved this value growth despite volume declines of five percent and three percent, respectively, reflecting the role of pricing in a tighter supply year.

In contrast, the ‘other apples’ segment grew in both value and volume, adding close to 5,000 tonnes to the sub-category, indicating strong consumer demand across managed varieties. Conversely, Royal Gala declined in both value (five percent) and volume (15 percent), highlighting increasing competitive pressure within the staple segment.

Apples in the wider fruit category

Despite reduced supply, apples demonstrated resilience within the broader fresh fruit basket.

There was a clear net value-shifting gain from berries ($4.4 million), which experienced their own supply shortfall during the year, as well as bananas ($1.4 million), which faced weather-related disruptions. This reinforces apples’ role as a reliable substitute when other fruit categories tighten.

In terms of purchasing volumes, grapes were the largest fruit category consumers switched to from apples, while modest net losses to citrus, stone fruit, and melons reflect normal seasonal rotation rather than a longer-term move away from the category.

Overall, apples remained a staple within the fruit basket, even in a year when supply was constrained.

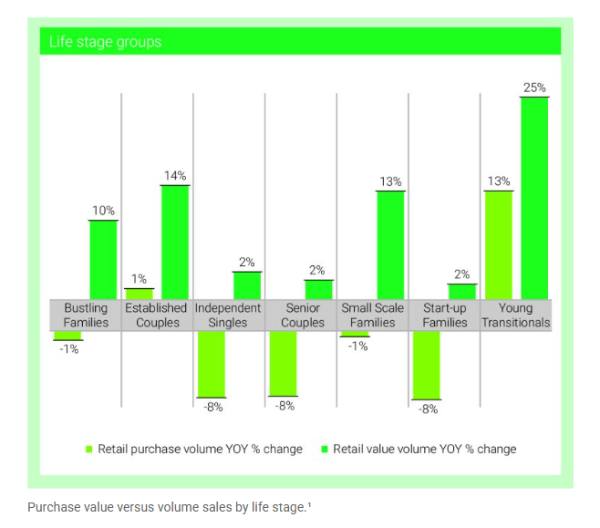

Who bought Australian apples in 2025?

APAL’s season analyses also looked into the consumer demographics driving apple sales in the country.

According to the report, Established Couples (ages 35 to 59; no children) and Small-Scale Families (families with older or fewer children at home) were the standout apple buyers.

Established Couples increased both value and volume, spending $12.6 million more at the checkout and contributing approximately 18 percent of the total apple category value in 2025.

Meanwhile, Small-Scale Families added a further $12.4 million, reinforcing the importance of family households to category performance.

Young Transitionals (younger than 35; singles or couples with no children) also delivered strong growth, adding $10.2 million in value alongside volume gains, indicating solid engagement from younger households.

Bustling Families (those with school-aged children at home) contributed nearly an additional $10 million, although they moderated volume slightly in a higher-price environment.

Senior Couples (ages 60+, no children at home) and Independent Singles (adults living alone; no children) made up 22 percent and 13 percent of category value. Both groups increased spending in dollar terms but reduced volume, suggesting greater price sensitivity and a shift toward alternative fruit such as bananas, citrus, and grapes.

The key takeaway is that Australian family households continue to underpin apple demand, while smaller and older households are more responsive to price movements in tighter supply.

What this means for the 2026 season

According to the industry body, grower interviews conducted during APAL’s 2026 crop forecast indicate a similar yield profile to 2025, with late-season heat again a major variable.

If supply remains tight, retail prices may remain elevated, but this will depend heavily on the availability and competitiveness of other fruit staples such as berries and bananas throughout the year.

If competing fruit categories return to stronger supply positions, apples may face greater intra-fruit competition. Conversely, if supply across the fruit category remains variable, apples are well positioned to maintain their role as a staple within Australian households.

*All figures are in US dollars.

** All images courtesy of APAL.

Related stories

Australian summer fruit growers anticipate excellent season across all states

Innovative avocado scanner boosts sales and consumer confidence in Australia trial

Expert insights on how to build a successful premium Australian apple brand in China

Subscribe to our newsletter