Agronometrics in Charts: California production edges higher in 2026 as imports continue to shape avocado market dynamics

Each week, the series ‘Agronometrics In Charts’ examines a different horticultural commodity, focusing on a specific origin or topic and visualizing the trade market factors driving change. Check out our entire archive.

The United States avocado market continues to be defined by strong import growth and shifting supply dynamics, even as domestic production shows modest gains so far in the marketing year.

According to estimates from the US Department of Agriculture (USDA) Economic Research Service, California avocado production is expected to reach 330 million pounds in 2025/26, marking a one percent increase year-over-year. The crop remains heavily concentrated in Hass and Hass-like varieties, which account for approximately 94 percent of total output.

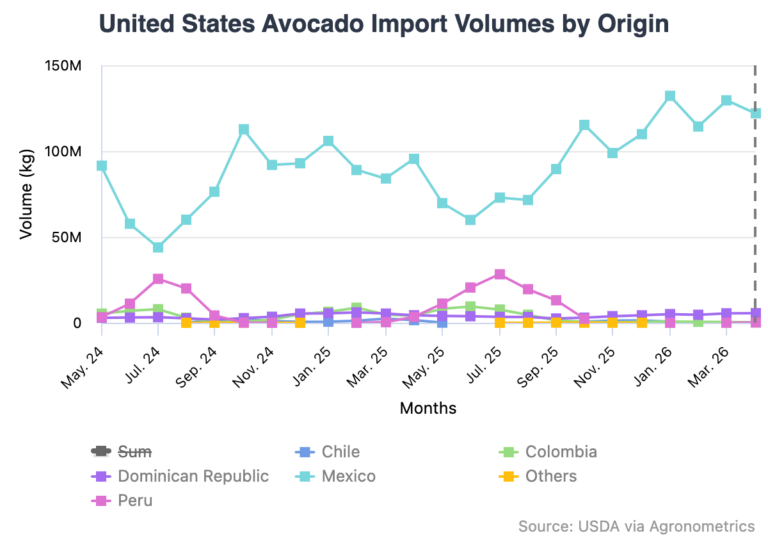

While California production is relatively stable, the broader US market continues to expand on the back of imports. In 2025, the United States imported a record 2.87 billion pounds of fresh avocados, up seven percent from the previous year. Mexico remains the dominant supplier, accounting for 83 percent of volume and 88 percent of value, with nearly all shipments consisting of Hass-type fruit.

Source: USDA Market News via Agronometrics. (Agronometrics users can view this chart with live updates here)

Seasonal shipment patterns continue to reinforce Mexico’s central role. Volumes typically peak in the winter months, with shipments reaching 92 million pounds in late January 2026, just ahead of the Super Bowl. Notably, shipments between January and mid-March were 24 percent higher than the same period in 2025, highlighting continued supply expansion.

This increase in supply has been accompanied by a shift in the distribution of fruit sizes. Larger avocados accounted for 50 percent of shipments this season, up from 40 percent a year earlier, reflecting improved growing conditions following the prior drought. However, the increase in larger fruit has placed downward pressure on prices. By mid-March 2026, FOB prices for larger Hass avocados from Mexico hovered near $1 per pound, roughly one-third of the levels observed during the same period last year.

Referential photo | Archive.

Additional competitive pressure comes from Peru and Colombia, which continue to expand their presence in the US market.

Peru supplied 218 million pounds in 2025, with shipments heavily concentrated in the summer months, overlapping with California’s peak season. During this period, lower-priced Peruvian fruit contributed to softer market prices. Colombia, while smaller in scale, reached record shipment levels and now accounts for approximately four percent of the US supply.

Domestic avocado market shows modest gains

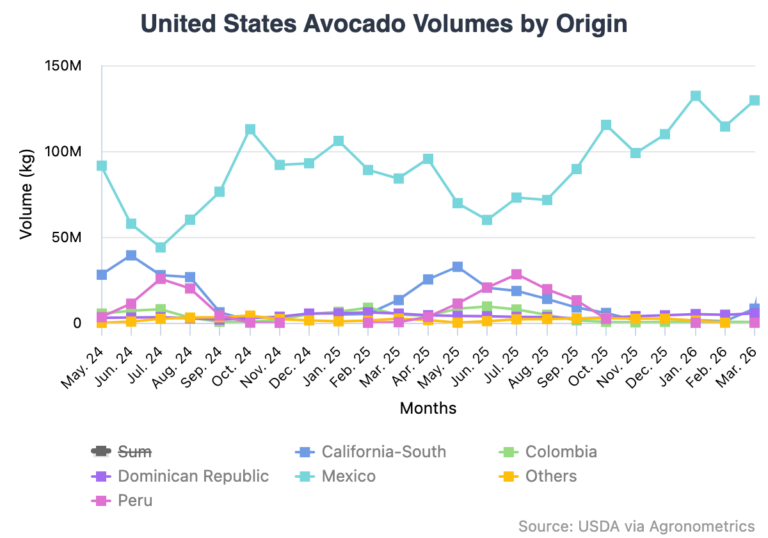

Against this backdrop, California’s 2026 season is off to a slower start.

As of mid-March, shipments represented just three percent of the projected crop, lagging the historical average of eight percent for this time of year. Higher import volumes and lower prices, particularly from Mexico, are likely contributing to delayed domestic movement.

Source: USDA Market News via Agronometrics. (Agronometrics users can view this chart with live updates here)

Looking ahead, California shipments are expected to ramp up through the spring, with peak volumes projected ahead of America's 250th. However, the interplay between domestic production and sustained import pressure will remain a defining factor for price formation and market balance throughout the season.

In an increasingly globalized avocado market, incremental gains in domestic production are being overshadowed by structural shifts in supply, where year-round availability and scale from key exporting countries continue to reshape competitive dynamics in the United States.

Related articles:

New Year’s drives 29 percent avocado unit sales growth

Post-game slowdown: Mexico still holds majority share of US avocado market

Avocado market finds balance as US volumes ease and China prices firm

Subscribe to our newsletter